Much has been written about the dramatic increase in income and wealth inequality in the United States over the last four decades. This volume of literature not only warns about the injustice of our current system, but also raises alarm that extreme inequality poses a serious risk to our democracy.

Concern about inequality is at least as old as the United States itself. Writing in 1792 about the necessity and dangers of political parties, James Madison made the connection between excessive wealth and its political influence:

The great object should be to combat the evil: 1. By establishing a political equality among all. 2. By withholding unnecessary opportunities from a few, to increase the inequality of property, by an immoderate, and especially an unmerited, accumulation of riches. 3. By the silent operation of laws, which, without violating the rights of property, reduce extreme wealth towards a state of mediocrity, and raise extreme indigence towards a state of comfort.

Excessive wealth concentration, in Madison’s view, was as poisonous for democracy as war. “In war,” he continued, “the discretionary power of the executive is extended; its influence in dealing out offices, honors, and emoluments is multiplied. . . . The same malignant aspect in republicanism may be traced in the inequality of fortunes.”

Wealth is power. An extreme concentration of wealth means an extreme concentration of power: the power to influence government policy, the power to stifle competition, the power to shape ideology. Together, these amount to the power to tilt the distribution of income to one’s advantage. This is the core reason why the extreme wealth of some can reduce what remains for the rest—why part of the income of today’s superrich can be earned at the expense of the rest of society. That’s what earned John Astor, Andrew Carnegie, John Rockefeller, and other Gilded Age industrialists their epithet of “Robber Barons.”

In much of the twentieth century, the U.S. tax system protected against such extreme disparities. But far from curbing this trend, the tax system in the last four decades has instead reinforced it. The three traditional progressive taxes—the individual income tax, the corporate income tax, and the estate tax—have all weakened. The top marginal federal income tax rate has fallen dramatically, from more than 70 percent every year between 1936 and 1980—in fact, often higher, peaking at 94 percent during the final years of World War II—to 37 percent in 2018. (The income threshold at which this rate kicked was several million of today’s dollars.) Corporate taxes—which are progressive in the sense that they tax corporate profits, a highly concentrated source of income—have declined from about 50 percent in the 1950s and 1960s to 16 percent in 2019. And estate taxes on large bequests are now almost negligible due to a high exemption threshold, many deductions, and weak enforcement.

A renewed political demand calls for progressive taxation to reverse these trends—to achieve greater tax justice, raise revenue to pay for important public goods, and curb the rise of inequality. Indeed, two major presidential candidates have proposed wealth taxes. In January 2019 Elizabeth Warren proposed a progressive wealth tax on families or individuals with net worth above $50 million with a 2 percent marginal tax rate and 3 percent above $1 billion (she revised that to 6 percent rate for billionaires in the fall). And in September 2019 Bernie Sanders proposed a similar wealth tax starting at $32 million with a 1 percent marginal tax rate, rising to 5 percent for billionaires and 8 percent for deca-billionaires. The key difference between these proposals and earlier proposals, for instance the one made by Edward Wolff in these pages (as well as existing or past wealth taxes in other countries), is the high exemption thresholds: fewer than 0.1 percent of U.S. families would be liable for the Warren or Sanders wealth tax.

Both presidential candidates rightly believe that a wealth tax of the sort they have proposed would fill a critical gap in the U.S. tax system: it would ensure greater tax justice by requiring that the ultra-wealthy pay taxes commensurate with their ability to pay. But in the long run, an ambitious wealth tax—with marginal tax rates high enough for billionaires—could also help address the threat that extreme inequality poses for democracy.

A wealth tax: the proper way to tax the ultrarich

Why isn’t the income tax sufficient for taxing the superrich? Because many of the most advantaged members of society possess substantial wealth but low taxable income. Maybe they own a valuable business that does not make much in profits, but which, everybody anticipates, will be immensely profitable in the future (think Amazon, before 2016). Or, as is more frequently the case, they may structure their already profitable business so that they generate little taxable income. Consider Warren Buffett. According to Forbes, Buffett owned $62 billion in wealth in 2015. We don’t know the exact rate of return on his wealth, but let’s assume it was 5 percent. On this conservative assumption, Buffett’s real pre-tax income—his share of his company Berkshire Hathaway’s profits—was $3.1 billion. That year Buffet paid federal income taxes of about $1.8 million, corresponding to an effective income tax rate of around . . . 0.058 percent.

Buffett’s effective income tax rate is so low because his wealth primarily consists of shares in his company Berkshire Hathaway, which does not pay dividends. When Berkshire Hathaway buys other corporations, Buffett forces them to stop paying dividends too. As a result, Buffett’s wealth has been accumulating for decades, free of individual income taxes, within his firm. Eliminating dividends and perpetually reinvesting profits boosts Berkshire Hathaway’s share price, year after year. One share now costs some $330,000, thirty times more than it cost in 1992. To finance any spending, Buffett need only sell a few shares. By selling forty shares, for example, he can move $13 million to his personal bank account. He then pays tax—a modest one—on the small amount of capital gains he just realized. And that’s the limit of his tax liability. Raising the top marginal income tax rate wouldn’t affect the tax bill of Buffett or Bezos notably, since neither of them has much taxable income in the first place.

That’s how billionaires such as Buffett, Jeff Bezos, and Mark Zuckerberg can live almost tax-free today. And that’s how the top 400 richest Americans have come to pay the lowest tax rate of any income group. When we combine all taxes at all levels of government (federal, state, and local), we find the U.S. tax system indeed now resembles a giant flat tax that becomes regressive at the very top. All groups of the population pay effective tax rates of roughly 28 percent, with mild progressivity up to the top 0.1 percent and a significant drop at the top—where effective tax rates fall to 23 percent for the 400 richest Americans.

What about corporate taxes? The 1950s U.S. tax system was highly progressive in large part thanks to very high effective corporate tax rates of about 50 percent. Those rates applied to profitable companies, which, at the time, had relatively few owners, typically individuals rather than institutional investors. Now, however, more than 20 percent of listed U.S. equities are owned by foreigners and 30 percent by pension funds, who accumulate assets on behalf not only of the wealthy but also of middle-class taxpayers. So even a massive hike in the corporate tax rate would not create the same degree of tax progressivity as the 1950s. The corporate tax is too blunt an instrument to restore tax justice.

Raising the estate tax also would not have the desired effect. Why should we wait for decades until today’s superrich Americans contribute to the public coffers? Neither a more progressive income tax, nor a higher corporate tax, nor a stronger estate tax would significantly address the lack of progressivity at the very top end of the scale. The way to address this problem is by taxing wealth itself, today and not at some long distant future date.

To be sure, a wealth tax will never replace the income tax. Top executives, athletes, or movie stars—who earn a lot of income but own relatively little wealth—can be appropriately taxed by a comprehensive income tax. The goal of a wealth tax is more limited: it is just one part of the strategy to ensure that the ultra-wealthy are taxed according to their ability to pay.

Taxing the superrich involves three essential and complementary ingredients: a progressive income tax, a corporate tax, and a progressive wealth tax. The corporate tax ensures that all profits are taxed, whether distributed or not: it acts as a de facto minimum tax on the affluent. The progressive income tax ensures high earners pay more. And a progressive wealth tax gets the ultrarich to contribute to the public coffers even when they, including Buffett, manage to realize little taxable income.

How to tax wealth: leverage the power of markets

A progressive wealth tax is possible because wealth is well defined at the very top, in contrast to realized income, which can be artificially reduced. Wealth is defined as the market value of one’s assets net of all debts. The taxable income Buffett reports to the Internal Revenue Service is a tiny amount of his true economic income; he is worth more than $50 billion. With a wealth tax at a rate of 3 percent for fortunes above $1 billion, Buffett would pay more than $1.5 billion a year.

Not all forms of wealth are as easy to value as Buffett’s shares in Berkshire Hathaway, and this has been a concern for critics of a wealth tax who believe it would be impossible to implement fairly. (A publicly traded company such as Berkshire Hathaway has a well-defined market value; because Buffett’s wealth is fully invested in Berkshire Hathaway shares, it is easy to tax him. But the affluent can also own shares in unlisted (also called private or closely held) businesses. Other forms of wealth—such as art or jewelry—are sometimes hard to value, too. But these concerns—as well as the claim that wealth taxation failed in many European states, so they must fail here—are often exaggerated. The valuation problems can be addressed, if there is political will to address them.

Here’s how. Modern capitalist economies such as the United States have well defined property rights and put value on most assets. Around 70 percent of the wealth owned by the top 0.1 percent richest Americans consists of listed equities, bonds, shares in collective investment funds, real estate, and other assets with easily accessible market values. For the remaining 30 percent—mostly shares in private businesses—valuation raises fewer problems than you might think. In the first place, shares in large private businesses—though not publicly listed—are regularly bought and sold. Even before Lyft and Uber went public in 2019, for instance, people could invest in the ride-sharing service companies. Private companies regularly issue new stock to banks, venture capitalists, wealthy individuals, and other “accredited investors” with sufficiently deep pockets. These transactions put a de facto value on private firms.

In some cases, however, no transactions take place for years, especially for mature private businesses controlled by a small number of owners. For example, 90 percent of the agribusiness giant Cargill, the largest private company in the United States, is owned by 125 or so members of the Cargill and MacMillan families. Cargill shares were last transacted in 1992, when 17 percent of the company’s shares were sold for $700 million—thus valuing the entire firm at a bit more than $4 billion. Here is a striking case where taxing wealth might seem hopeless. What is the value of Cargill today, almost thirty years after this last share transaction? Isn’t any estimate fraught with countless risks of abuse?

But in fact, taxing the Cargills and the MacMillans equitably is not impossible. To start with, the tax administration can take the 1992 Cargill valuation and update it based on any changes in the company’s profits since then. If the company makes three times more profits today, it is not unreasonable to believe it is worth about three times as much as in 1992. Of course, much more information ought to inform a reliable valuation. What sort of information? Data about Cargill’s direct competitors that are listed as public companies, such as Archer Daniels Midland and Bunge, for example. To better assess Cargill, the IRS can consider how much a dollar of earnings made by these firms is valued by the stock market. It can study how the price-to-earnings ratios of Archer Daniels Midland and Bunge have changed since 1992. Every day, hundreds of financial analysts value private firms in this, and more complex, ways. The United States, with its sophisticated financial markets, has no shortage of expertise in this area. Drawing on standard private sector practices, it would not be terribly complicated for the IRS to come up with a reasonable estimate of Cargill’s market value at the end of each year.

But suppose that the MacMillans and Cargills feel cheated by the IRS—they complain that the IRS, out of an interest in generating tax revenue, over-estimates the value of their firm. Perhaps Cargill has fundamentally changed since 1992, in ways that state-of-the-art valuation techniques may fail to capture. Perhaps it has weaknesses that its competitors do not share. What is to be done?

The heart of the problem is a missing market: while there is an active, liquid market for Archer Daniels Midland and Bunge shares, no such market exists for Cargill’s stock. The solution to this problem, in our view, is for the government to step in and create the market that is missing. The IRS would give the option to Cargill’s shareholders to pay the wealth tax in kind—with Cargill shares—rather than in cash. If they used this option (which they would do only if they believed the IRS valuation was exaggerated), the tax authority would then sell the shares to the highest bidders on a market open to any and all bidders—venture capitalists, private equity funds, foundations, or other rich families interested in acquiring a stake in the agribusiness giant.

This solution addresses the challenge head on. Just as a well-functioning income tax should treat all income equally, a good wealth tax should treat all assets in the same way, at their current market value. If some values are missing, the solution is to create them. And there is nothing better to create a market value than, well, to create a market. For a wealth tax imposed at an average rate of 2 percent, Cargill’s shareholders would hand in 2 percent of their shares each year (or the cash equivalent, if they prefer to retain full control of the company). As with Buffett’s Berkshire Hathaway, there would be no getting away. Transforming Cargill’s shares into cash would be the government’s job.

This solution also addresses another frequent objection to wealth taxation—the problem of liquidity. Very rich people may have a lot of wealth and yet not enough income to pay their tax bills. Isn’t it unfair to force them to pay a tax when they don’t have cash in hand? To be frank, liquidity concerns are often put forward in bad faith. The claim that people worth hundreds of millions of dollars may not have enough cash to pay a million dollars in tax does not often withstand scrutiny. If ultrarich individuals say they have little cash, it is usually because they choose to realize little income to avoid the income tax. They organize their own illiquidity.

But suppose the liquidity problems are real. The most relevant case might be a highly valued startup that makes no profit. Generating cash each year may turn out to be complicated or costly for anyone whose primary source of wealth is shares in the company, since young firms typically do not pay dividends. In that case, allowing taxpayers to pay in kind—with shares of the companies—addresses the problem. Because the wealth of the rich mostly consists of equity, and equity (in contrast to real estate) can always be divided, it can be used to pay for the tax. If the wealth tax can be paid with assets rather than cash, a progressive wealth tax isn’t harder to implement in practice than a progressive income tax.

The middle class already pays taxes on its wealth, in the form of property taxes. The wealthy don’t, since most of their wealth consists of financial assets, which are exempt from the property tax. In the nineteenth century, by contrast, the property taxes of most states fell on all assets, both real and financial. In the beginning of the twentieth century, the United States pioneered the progressive taxation of property with its federal estate tax—now moribund. Before turning its back on this distinguished tradition, the United States was at the forefront of the democratic regulation of property via the tax system.

Curbing wealth concentration: a radical wealth tax

From 1930 to 1980 the top marginal income tax rate in the United States averaged 78 percent; it exceeded 90 percent from 1951 to 1963. These quasi-confiscatory top rates championed by Franklin Delano Roosevelt and his successors in office were meant to reduce the income of the superrich: not simply to achieve tax justice, but to compress the income distribution. These tax rates applied to extraordinarily high incomes only, the equivalent of more than several million dollars today; only the ultrarich were subjected to them. In 1960, for example, the top marginal tax rate of 91 percent started kicked in at an income threshold that was nearly 100 times the average national income per adult, the equivalent of $6.7 million in income today. The merely rich—high-earning professionals, medium-size company executives, people with incomes in the hundreds of thousands in today’s dollars—were taxed at marginal rates in a range of 25 percent to 50 percent, in line with what is typical nowadays (for instance, in states such as California and New York, when you count state income taxes).

According to the evidence, the policy of quasi-confiscatory tax rates for sky-high incomes achieved its objective. From the late 1930s to the early 1970s, income inequality fell. The share of pre-tax national income earned by the top 1 percent was reduced by a factor of two, from close to 20 percent on the eve of World War II to barely more than 10 percent in the early 1970s. In 1960, for example, only 306 families earned more than $6.7 million in taxable income a year (the threshold above which income was imposed at 91 percent).

This tax policy reflected the view that extreme inequality hurts the community; that the economy works better when rent extraction is discouraged (indeed, the economy grew strongly in the mid twentieth century); and that unfettered markets lead to a concentration of wealth that threatens our democratic and meritocratic ideals.

Extreme wealth concentration, like carbon emissions, imposes a negative externality on the rest of us. The point of taxing carbon is not to raise revenue but to reduce carbon emissions. And the point of high tax rates on the very highest incomes is not fundamentally to fund government programs. They are aimed at reducing the income of the ultra-wealthy. The reason for reducing those incomes is not, as critics sometimes say, to give vent to envy. It is to disrupt privilege, impede rent extraction, and protect democracy. When 90 cents out of any extra dollar earner will go to the IRS, we will disincentivize negotiating a $20 million salary, earning millions by creating a zero-sum financial product, and spiking the price of patented drugs. Quasi-confiscatory tax rates equalize the distribution of pre-tax income, make the market place more competitive, and limit the concentrations of economic power that pave the way for undemocratic concentrations of political power.

To see how wealth taxation might work to reduce such concentrations of wealth and power, let’s contrast a moderate with a radical wealth tax.

A moderate wealth tax, say with marginal tax rates of 2 percent above $50 million and 3 percent above $1 billion, would generate a lot of revenue—about 1 percent of GDP each year, according to our estimates.

Consider now a more radical wealth tax with a marginal tax rate of 10 percent above $1 billion. A person with $1 billion in wealth would pay the same $19 million as under a moderate wealth tax. A radical wealth tax would not make it harder to become a billionaire; it would make it harder to remain a multi-billionaire. A person with $2 billion would pay almost 5 percent a year, a decabillionaire such as David Geffen 9 percent, and a centibillionaire such as Bezos 10 percent (instead of 3 percent with a moderate wealth tax). Just as Roosevelt’s 90 percent top marginal income tax sharply reduced the number of families earning more than $10 million of today’s dollars, a radical wealth tax would eventually lead to a reduction in the number of multi-billionaires. More than collecting revenue, it would de-concentrate wealth.

A wealth tax to limit the rise of inequality… or de-concentrate wealth?

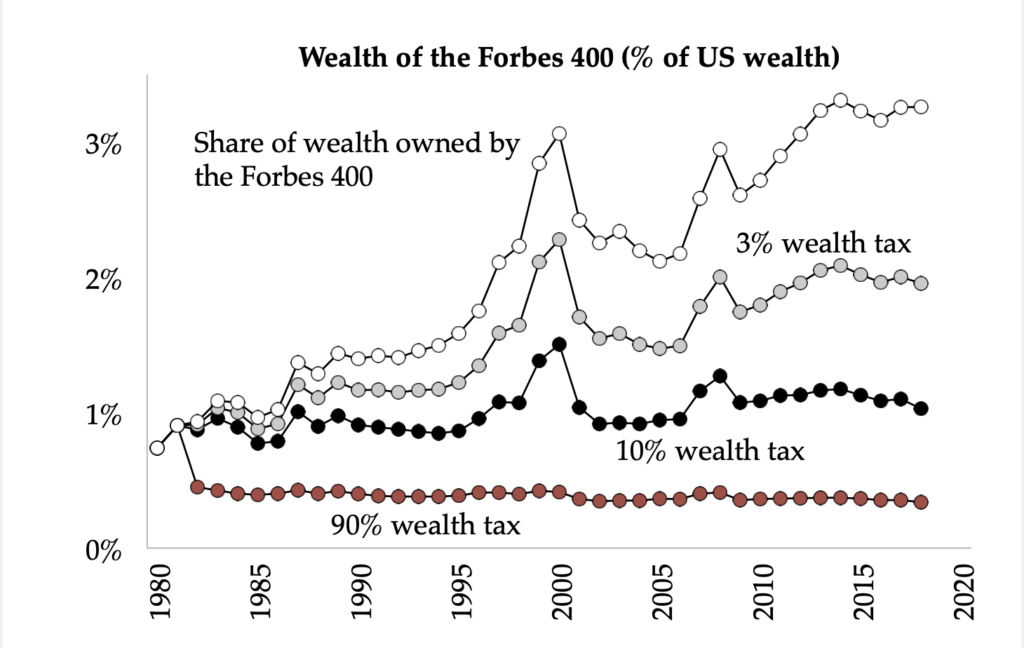

(Forbes 400 share of total wealth actual vs. with wealth taxation since 1982)

There would still be multibillionaires, no doubt. If a wealth tax of this higher sort had been in place over the last decades, Zuckerberg would still be worth $21 billion in 2018—instead of the $61 billion recorded by Forbes. Why? Because Zuckerberg’s wealth has grown at a rate of 40 percent a year since 2008 when he first became a billionaire. A 10 percent annual wealth tax would not have stopped his stratospheric ascent. But a more mature billionaire such as Bill Gates would be worth “only” $4 billion—instead of $97 billion in 2018—because he has been a billionaire for over three decades now, giving the radical tax more time to reduce his wealth. If a radical wealth tax had been in place since 1982, most of the 400 richest Americans would still be billionaires in 2018, but they would be only one third as wealthy as they currently are (see graph 1). Their share of U.S. wealth would be similar to what it was back in 1982, before the wealth inequality took off.

A radical wealth tax would have raised $250 billion in revenue from the 400 richest Americans alone in 2018. That is more than 1 percent of GDP. But if such a tax had been in place since 1982, it would have only raised $66 billion from the 400 wealthiest families in 2018, while a moderate wealth tax, despite its much lower rate, would have yielded almost as much—about $50 billion. In the long run, a radical wealth tax erodes top fortunes so much that it reduces the taxes paid by the ultrarich.

Is a radical wealth tax worth it, then? Would society benefit from curbing huge fortunes, even if it means lower tax collection at the top end? Over the years, our own thinking about this question has evolved as the stagnation of working-class income, the boom in extreme wealth, and the threats to democracy became clearer. Perhaps yours will too.

Independent and nonprofit, Boston Review relies on reader funding. To support work like this, please donate here.