“I wanted to go to college to avoid being a third-generation janitor.”

The man on stage at this California town hall tells a familiar story. He’s now a beloved high school principal, but to finance his education, he took out a loan—$80,000. First, repayment according to plan—a strain, but not impossible. Then, a medical catastrophe; default; bankruptcy. Next, depression; a second default; a debt nearly twice the volume of the original loan. It became a family affair: the man’s parents, cosignatories on the original ticket to the American dream, now bear the consequences of its falling through. They may see their wages garnished, he reports, their social security under lien. Sympathy rises up, palpable, from the crowd.

The town hall is a presidential campaign event for Bernie Sanders. On June 24 Sanders announced his intention to cancel all $1.6 trillion of outstanding student loan debt, following Elizabeth Warren’s proposal for more limited cancellation in April; three months later he announced the same for medical debt—$81 billion in 2016, carried by an estimated one in six U.S. adults. Here there are even more gruesome facts behind the figures: single mothers, sick elders, sued for unpaid medical bills, in foreclosure for unpaid medical bills, arrested for unpaid medical bills.

Today the phrase “debtors’ prison” is often invoked to describe this experience of punitive indebtedness. Sometimes it is meant literally. Consider Melissa Welch-Latronica, a thirty-year-old single mother, who in February was wrenched from her minivan and thrown into a jail cell in Porter County, Illinois, over failure to pay an ambulance bill. Her story is unusual but not unique. A 2018 ACLU report documented a thousand cases of the “criminalization of private debt” and compiled a dozen of the most extreme stories. Most of the people featured ended up in jail because they failed to appear in court over unpaid debts, resulting in a warrant. And then there is the abominable, systemic cycle of incarceration and reincarceration of poor people—and particularly poor people of color—unable to pay fines and court fees.

Still, the debtors’ prison as such—a prison specifically for the detention of those unable to pay their private debts—is long gone. The more common experience resembles that of the California principal: punitive collection takes the form of liens, garnishments, and foreclosures. For most, the story ends not in detention but in default and bankruptcy—possibly homelessness, or impossible choices between food, shelter, medicine, and payment.

The abolition of the debtors’ prison figures in a larger evolution of debt in America. Moral laws derive their power from a sense of natural order. But in moments of crisis, when insolvency has become the norm, the morality and mathematics of debt have proven fungible, susceptible to thoroughgoing change. We may look to this history for hints of how the moral calculus of debt might be poised once more for transformation—and for confirmation that what appears as common sense today could be deemed cruel and unusual tomorrow.

That the meaning of debt can change radically is evident from the changes it has already undergone, even before it reached North America. Debt didn’t always suggest collection agencies and APRs; the earliest evidence of credit relations, dating to Sumerian city states around 5,000 years ago, signified something quite different. In his sweeping history Debt: The First 5,000 Years (2011), the anthropologist David Graeber suggests that cohesion in the earliest societies would have grown out of a sense of divine, unpayable indebtedness and an expectation of mutual reciprocity. For most of human history, this was the kind of indebtedness most people would have recognized: an “everyday communism,” Graeber calls it, of collective stewardship and interdependence without end.

Graeber’s central claim is that the rigid state apparatus for the regulation of indebtedness—the development of state-sanctioned money, a regime of quantified exchange, and punishment of nonpayment—had to be created, predicated on the fungibility of debt. And for Graeber, an anarchist, it can just as well be dismantled. Contemporary debt’s moral foundations—the idea that failure to pay a debt is a profound misdeed or moral failing, and that a creditor’s entitlement to repayment with interest trumps all other obligations—are just as historically contingent as the coercive institutions they support. With the global movement of slavers under a mercantile, imperialist paradigm, Graeber contends, the borders of communities contracted to surround individual bodies or familial units; the currency-based trading that had long taken place at the edges of society came to dominate exchange within it. At a certain point in history, almost everyone became a stranger.

The cultural critic Lewis Hyde has traced that estrangement to the Reformation in Europe, at which point Christian laws surrounding usury—neither a borrower nor a lender be—adapted to a new global reality. Usury had always existed on the fringes of Christian society, most famously the dominion of the Jews, whose outsider status could be strategically deployed to allow both violence and the kind of enterprise lending that helped capital circulate and general wealth increase. But in the sixteenth century, John Calvin argued that, because borrowed money increased value for the borrower, returning some of that value to the lender in the form of interest was the most just act. Martin Luther likewise reasoned that though it was Christian to forgive debts, true Christianity was not viable within a tainted civil sphere; thus it was just and right for the state to rigidly enforce the rules of debt—a thin line between society and barbarity.

In 2019, anyone with a monthly credit card bill can recognize the foundations of the modern economy in Calvin and Luther’s principles. But their injunctions have not endured unqualified. A sense of innate interpersonal indebtedness—Graeber’s everyday communism, or what Hyde calls the “circle” of mutual obligation—still rules in many of our most intimate relationships, if not in the marketplace at large. Meanwhile, the existence of bankruptcy protections suggests that our modern economy depends, to some extent, on exceptions—on the abiding fungibility of debt.

When Europeans crossed the Atlantic, they brought with them the unforgiving Reformation conceptions of debt. At the beginning of an age of imperial expansion, as Graeber describes, kings and conquistadors found themselves so deep in the hole that they went halfway around the world to dig themselves out of it—or, rather, to force the enslaved and indentured to dig them out, destroying entire civilizations in the process.

In other respects, though, economic life in parts of early colonial America resembled tribal sustenance more than brutal commercial exchange. In seventeenth-century Connecticut, for example, economic and legal relationships among free citizens were informal, governed by “book debts”—tabulated records of who owed what—as well as by what the legal historian Bruce Mann (incidentally, Elizabeth Warren’s husband) calls a “communal model” of dispute resolution. As Mann describes it in his study Neighbors and Strangers (1987), trust remained at the core of the relationship between creditors and debtors. Book debts didn’t signify formal promises to pay, but rather an understanding that payments would be made as the debtor became able. Credit was extended through personal connection, and disputes were negotiated through appeals to personal character.

Communalism does not preclude conflict, of course; disputes were common. But only after informal, interpersonal dealings had deteriorated would matters come before the courts. There, character witnesses would testify, and recorded book debts would serve only as a starting point for discussion about who owed and how much. Still, the number of debt cases heard by local courts, Mann argues, points to the importance of credit in a young, cash-poor society. As Mann went on to explore in Republic of Debtors (2002), the same was as true for the relatively wealthy as for subsistence agrarians. In the land of self-made merchants, debt was a way to get money flowing, especially when the money itself—gold and silver—was thin on the ground. At first this debt was governed by its own kind of communalism—what Graeber calls the “communism of the rich.” Among the Southern plantation and Northern merchant classes, it was gauche to demand repayment of debts—a rupture of gentlemanly agreements. Equilibrium meant most debts were eventually repaid.

This communalism would be short-lived; timely repayment would soon become an inviolable economic principle. Mann’s archival work shows that an informal economy of debts, anchored in and inflected by personal relationships, existed as late as the 1720s in rural Connecticut. Within a generation, though, it had given way to the “cold specificity” of bonds and promissory notes. The reason, Mann contends, was increasing population diversity. Paper representations of debt—so-called “scrip”—could facilitate exchanges with unknown actors. It wasn’t long before such promissory notes began to circulate. As collectivities of neighbors gradually became collections of strangers, new forms of debt policing crowded out older forms of tolerance, and the communitarian legal culture of early colonial life morphed into the adversarial, litigious mess we know today.

The mercantile class also found use for paper debts, which eventually became the object of profitable speculation. High-value notes could be auctioned and “assigned,” ranging further than the relationships they had originally represented and depersonalizing debt in the process. As a result, debts were collected with greater frequency and fervor. With economic contractions like the one that followed the Revolutionary War, note-holders became less inclined to trust borrowers, and more concerned about the depreciating value of the paper they held. Decorum among the merchant classes dissolved.

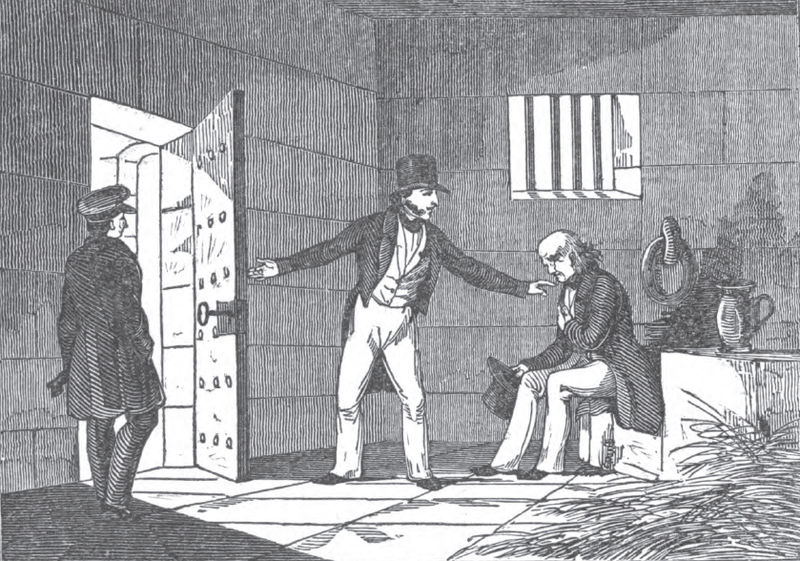

In the background lurked the threat of debtors’ prison. Formerly a more typical fate of the truly destitute, by the late eighteenth century debtors’ prisons brimmed with “respectable” folk. Commonplace though debt had always been, it remained a shameful thing, a mark of unmanly dependence on the generosity of others. (Southern plantation owners especially resented how indebtedness to British creditors seemed to align them with the enslaved people on whose backs they were attempting to build their fortunes.) Imprisonment for insolvency was the greatest indignity of all. When the system of gentlemen’s agreements began to falter and debt collectors came knocking, the effects were felt most acutely by those at the end of the chain of debt—farmers such as those who led Shay’s Rebellion in rural Massachusetts, who rose up against debt collectors when threatened with the seizure of their belongings and land for failing to produce specie. But as debtors’ prisons became the dominion of the well-to-do, the social narrative of debt had to shift in order to resolve the incongruity.

What’s more, imprisonment for debt didn’t much help the insolvent repay their debts—which was, at least in theory, the whole point of detaining them. For traders, debtors’ prison was meant not as punishment but as a form of financial security, holding the delinquent in place until their balances were restored. But with silver and gold no more readily available than before, there was often little an imprisoned debtor, deep in the hole, could do. Many well-known colonial insolvents spent their days writing impassioned letters from prison, begging for clemency. Fiery broadsides posited merchant debtors as either noble economic pioneers, or else victims of happenstance. War-triggered recessions made it obvious that insolvency could befall businessmen through no moral “fault” of their own. Debt thus gradually came to be seen as an economic, rather than personal, failure. Prisoners of status fashioned themselves as upright citizens, and their debts as a feature of entrepreneurial citizenship. In stark contrast to today, debtors and creditors alike found themselves working as peers and partners toward resolution.

Resolution of that incongruity would come in the form of the federal Bankruptcy Act of 1800. At that time, bankruptcy was the sole provenance of commercial debtors, the mark of legitimate risk and noble failure. But even this partial concession signaled a stark transition in public conceptions of debt. It marked a significant break with the old Reformation mentality that all debts must be repaid at all costs, creating a category of forgivable debts that has been the subject of negotiation and debate ever since. (Today student loans are still usually ineligible for discharge through bankruptcy.) It marked, too, the point of no return in the creation of an economy based on debt, speculation, and interest, as well as the acceptance of a paradigm that modern-day economics take for granted: booms require busts.

Throughout the century that followed, busts were plentiful, encouraged by the instability of the decentralized banking system and the rapid expansion of credit. To be American was to imagine oneself an entrepreneur. When bank-antagonist Andrew Jackson resisted calls for a central currency, private, state-chartered banks proliferated and issued their own, highly flammable banknotes; periodic panics found banks unable to redeem paper for specie, leaving note holders emptyhanded when collectors came calling. When Jackson mandated cash-only land transactions in the West, an 1837 run on the banks triggered the one of the worst economic crashes in U.S. history. “Thousands who had fondly dreamed themselves millionaires, on the point of becoming such, awoke to the fact that they were bankrupt,” wrote New York City newspaper editor and politician Horace Greeley.

As debt proliferated, so too did cultural ambivalence about its meaning. According to Philip Gura’s study of antebellum moral philosophy, Man’s Better Angels: Romantic Reformers and the Coming of Civil War (2017), many nineteenth-century social theorists were troubled by the effect of credit on the country’s social fabric, even beyond the explosions of bankruptcy and unemployment that followed bank failures. Some viewed the paper economy as a “perverse” order, conjuring a smoke-and-mirrors equivalency between a bank note and a bushel of wheat. Others saw the depersonalized paper economy giving rise to corruption. Albert Brisbane, a utopian socialist, wrote of debt instruments as “schemes and artifices,” condemning “a restless money-making spirit, and the cupidity and selfishness which arise from the action of isolated individuals and companies” as fertile ground for fraud. Yet many reformers also saw the potential fruitfulness of a paper economy for the new nation, and imagined utopian social orders that incorporated it.

William B. Greene, a theologian and social theorist associated with the Transcendentalist movement, railed against shiftless bankers, echoed the French anarchist Pierre-Joseph Proudhon in declaring that “property is theft,” and condemned the growing distance between capital and labor. Yet Greene was not a socialist; he believed that centralized economies and state interference in private life constituted an affront to freedom. Instead, he thought that liberty and God’s design could only be realized through a free-flowing and competitive market economy that dispensed with usurious banks. (To Greene, this economic system took the form of mutual banking, which he believed could preserve the expansive possibilities of paper alongside communalist values, with lenders charging only nominal interest rates and currency divorced from hoardable specie.) Horace Greeley, meanwhile, loathed the alienation and atomization of an economy based on individual self-interest, but saw industriousness as a moral imperative, and found the emergent capitalist system inefficient and wasteful, as well as exploitative. Greeley favored the concept of “association” developed by the French utopian socialist Charles Fourier: economic cooperation, blended with a nationalized banking system, would increase collective wealth and bring capital and labor into harmonious alignment.

If some of these ideas ring a familiar bell today, they have also never been so remote. The Civil War, Gura argues, stopped these alternative visions in their tracks. What took shape in its aftermath—the vastly unequal, exploitative, industrial economy of the late nineteenth and early twentieth centuries—confirmed these idealists’ worst fears.

As well as prefiguring the dangers of a speculation-based economy, the debt crises of the 1800s also helped crystallize the new morality of debt, in the form of expanded bankruptcy protections. In 1841 federal legislators extended bankruptcy laws to all borrowers. Within two years some 41,000 people had filed for bankruptcy. Within four, the federal law had been repealed, but the principle was in place: states continued to offer bankruptcy protection, and eventually debtors’ prisons would be gone for good. The debt economy was here to stay. The issuance of the first federal “greenback” currency in 1862 and the establishment of the Federal Reserve in 1913 bookended a period of dramatic growing pains, in which state and federal governments wrestled for supervision over banks, lending, and currency, cementing the role of commercial debt in economic growth.

It wasn’t until after World War I, however, that it became legal for banks to lend to individuals for profit, marking a final turn towards the economy of debt that we recognize today. As the economic historian Louis Hyman relates in Debtor Nation: The History of America in Red Ink (2011), for the low-waged industrial working-class, debt was an unavoidable part of life. Though capitalists, in practice, had long been able to secure personal loans from the banks that funded their industry, the workers who powered the mills and factories paid loan sharks breathtaking interest rates to make ends meet. Working-class consumers and retailers alike relied on informal systems of credit similar to the book debts that had driven local economies in colonial Connecticut, but the transition to a commercial, paper-based economy had wrought an irreversible change in the social function of debt.

Rather than the collective stewardship of a community built on mutual obligation, these book debts were a resentful byproduct of “competition”—credit captured more customers, but also risked losing money to unreliable borrowers. To protect borrowers and merchants alike, by the late 1910s and early ’20s, laws regulating small loans finally made consumer lending a legitimate and profitable business. Automobile financing soon followed, along with a flurry of further regulations and a massive home-ownership lending push in the wake of the Great Depression. It was off to the races.

In the twentieth century, American economic citizenship thus came to mean a right to debt (for borrowers) and a right to interest (for lenders). Indeed, equal access to credit would become a major rallying cry for midcentury antidiscrimination movements. But what had been marketed as opportunity transformed into obligation. As Hyman describes, by the end of the century, nonparticipation in the credit economy was no longer possible; every American adult was assigned a credit score, and the apparent self-sufficiency of a so-called “middle-class” life became accessible only by climbing that ladder of financialized debt. It was financial institutions’ hunger for growth that led debt to metastasize into every corner of American life.

The key driver of this metastasis was securitization: the bundling of concrete debts such as mortgages into a new kind of commodity that, however ephemeral, could be bought, sold, and insured for profit, and which was utterly anonymous, requiring basically no knowledge of the component debts themselves. Though the manipulation of this complex web of bundling, reselling, and selective blindness would eventually trigger the 2008 financial crisis, the mechanism actually originated with efforts to stimulate capital markets for expanded home-ownership and economic development amidst post-industrial urban decline.

In the process, banks developed what Hyman calls an “alchemical science of turning assets into securities,” by which, “with the right math, a mortgage could be turned into anything.” As the same method was adopted and refined on the credit card market between the 1970s and the 1990s, anti-regulatory politicians and banking interests systematically dismantled the post-Depression regulations that had separated investment and consumer banking. The repeal of the Glass-Steagall act in 1999 implicated more and more of the economy in speculative game-playing, and, according to the economist Joseph Stiglitz, allowed the high-risk, returns-driven culture of investment banking to rein supreme.

As it had in the paper crazes of the nineteenth century, debt itself became the money-maker—but for lenders, this time. With credit cards, rather than preventing a loan from being made—as bad “credit” might have between acquaintances in colonial Connecticut—a borrower’s heavy debt burden came to suggest a different pathway to payoff. Lending institutions built their growth models on increasing the total consumer debt by any means necessary—including and especially extending credit to those who likely would not be able to pay back what they owed. Meanwhile, stagnant wages inverted the relationship between how much debt a person carried and how much they were expected to pay back. By the end of the twentieth century, Hyman argues, the expansion, buying, and selling of debt had become a primary engine of capital creation in the U.S. economy. Individual debt burdens rocketed to record heights.

Beginning in the 1990s, spiking bankruptcy rates invited a return to Reformation-style moralizing. The expansion of credit cards into markets previously deemed too “risky” racialized the profile of consumer credit, and racist tropes could be mobilized to contain the moral responsibility of defaults. (Racial inequities still dictate whom debt burdens the most, and who best accesses debt’s purported dividends.) Fretting about how all that debt would ever be repaid remained constant, but abstract; for the most part, debtor-creditor synergy continued undisrupted. Living with debt seemed normal. There was a sense of process, of getting what you pay for on the installment plan.

Until 2008. Like Shay’s farmer rebels, mortgage holders suffered the shattering of a fragile economy built on deferral. It was the incongruity, perhaps, of the collision of home ownership—that surest of bets, that emblem of security—with the sudden dissolution of the debt pact. Or maybe it was the fact of homes in the balance that made a marketplace of basic needs, premised on risk and available only to risk-takers—with profits for the lender guaranteed—begin to appear, once more, morally suspect. When debtors filled Zuccotti Park in 2011, they levied a damning and credible charge: lenders did this, they did it knowingly, and they did it for profit.

It is telling that Graeber and Hyman published their studies of debt in 2011, riding the same wave that powered the Occupy movement. More than a decade after the seismic crash that triggered it, the full force of that wave has yet to break. Debt burdens and default rates both are on the rise. But our own cultural ambivalence around debt remains unresolved. To some, the indebtedness of modern Americans illustrates a national value system in positive terms—the desire to dream big. Yet consensus seems finally to be taking shape: our indebtedness cannot be sustained.

Dissolving debts en masse would have been unthinkable to a seventeenth-century butcher or an eighteenth-century merchant, but within a century, the calculus had utterly transformed. Debt today is clearly very different. Yet the transformation underway in the public moral discourse of debt—the status of the individual debtor and the institutional creditor, not to mention the entire profit-making enterprise—invites comparison.

While insolvency had become a universal accident by the end of the nineteenth century, today it is emerging as a universal harm. It is not a calculated choice, and not a personal failure, but something done to individuals by a faceless creditor conglomerate with vastly more power. Debts today implicate everyone—as grist for the economic mill, they are everybody’s problem—but they are also anonymized and abstracted, a far cry from the collective stewardship that circulating debt might once have propped up.

Graeber writes that debt has usually been a “peculiar agreement between two equals that they shall no longer be equals, until such a time as they become equals once again.” Certainly this was true for many economic citizens of New World agricultural settlements and mercantile enterprises. But under a professionalized and inescapable for-profit debt administration, there is only hierarchy maintained by an illusion of future equality, and that illusion is failing.

The vestiges of shame that still circled the indebted are finally falling away. (Slowly, still—much of the rhetoric around student loan and medical debt makes implicit value judgments and distinctions between different kinds of debt. College students and sick people are virtuous, in these accounts, while people struggling with credit card debt may not be.) Organizations such as Strike Debt!, which arose in the aftermath of Occupy, called for broad resistance to all kinds of private lending; their Debt Resistors’ Operations Manual (2014) details procedures and allies for the refusal to pay, from medical and student debts to mortgages and automobile payments.

They follow in a grand tradition, stretching back to Sumerian civilizations of 2400 BC. Hammurabi, the original lawmaker, decreed that all his subjects’ debts be forgiven four times throughout his reign, in response to widespread popular uprising. Debt is a social construction, fundamentally malleable, and what’s unmanageable must eventually be seen as immoral. But as debt becomes too heavy to bear, and as Americans find themselves at the end of a long road paved with false premises, a choice remains: to rebalance the scales, or to renegotiate the meaning of debt entirely.